I found the below analysis of the Apple Watch compared with the WHOOP fitness wearable to be a gold mine, with 4 big ideas that tee up 2 paradoxes AgTech companies face.

(1) Specificity can create big markets:

(2) Market clarity impacts everything about the product:

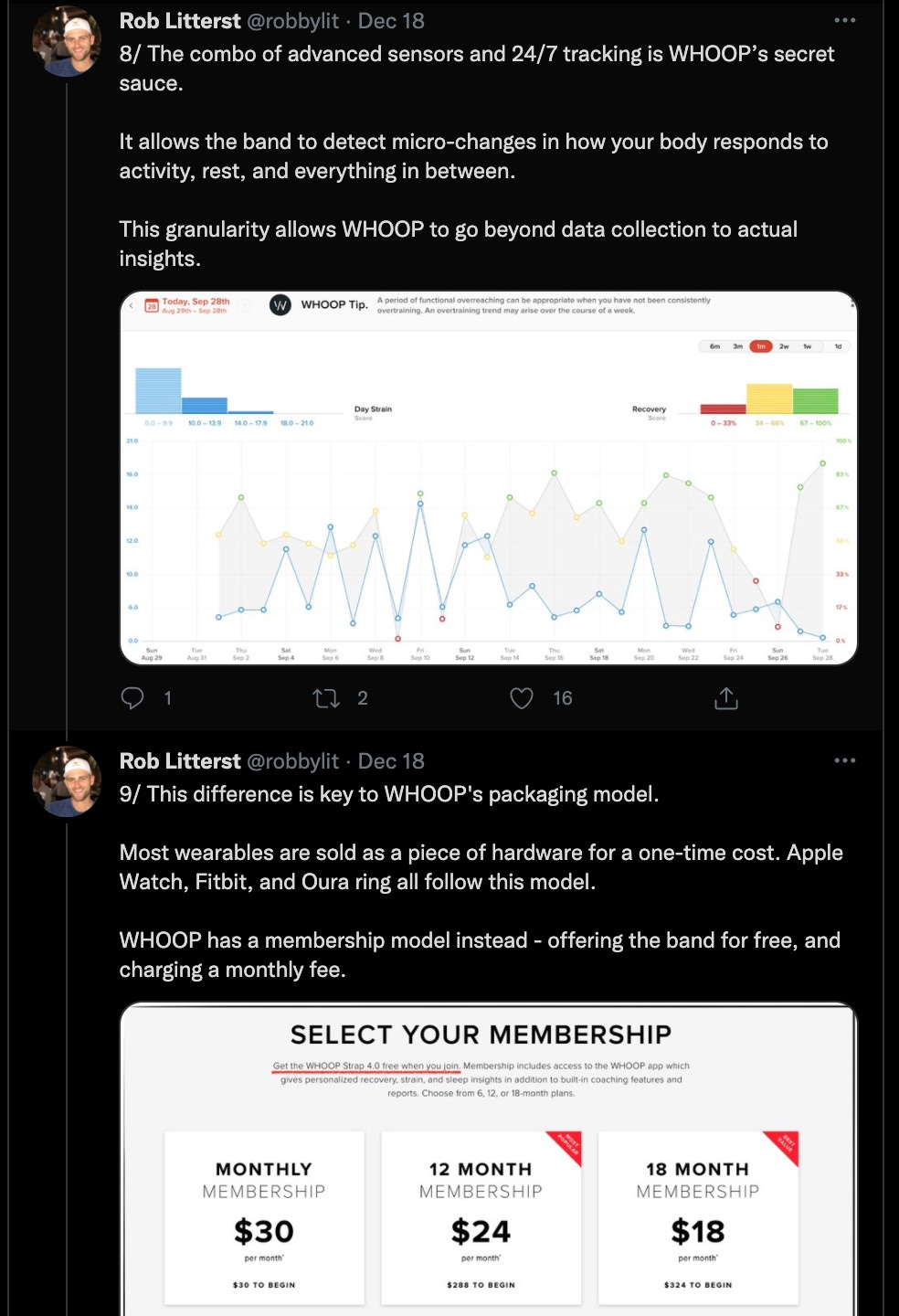

(3) Product-market clarity impacts business model:

(4) Product-market clarity increases value creation:

That’s what a rando outsider sees; here’s what Whoop has to say about themselves:

“Your 24/7 personalized fitness and health coach.”

“WHOOP 4.0 – the latest, most advanced fitness and health wearable available. Monitor your recovery, sleep, training, and health, with personalized recommendations and coaching feedback.”

Let’s go ahead and call WHOOP a really great example of product-market clarity.

(In the tech world we talk all the time about finding product-market fit, but I wonder if product-market clarity makes it easier to find product-market fit. Whether product-market clarity is a leading or lagging indicator to product-market fit is a debate for another day though.)

Now let’s contrast WHOOP with Agtech companies who talk about solving macro, world-saving, how-would-humanity-continue-without-us types of problems. I’ve never once heard a producer lament those problems though; producers don’t typically have a…

- pressing need to feed the world

- generic, burning need for analytics

- acute lack of artificial intelligence or machine learning or blockchains

- dire need for transparency

And yet that kind of grandiose-but-vague language is all over websites and marketing materials in the ag industry, particularly from agtech startups.

On the other hand, I have heard many a producer talk about the ongoing struggle with questions like:

- how do I access premium markets?

- how do I increase predictability of cash flow?

- how do I reduce medication costs?

- how do I manage rising labor costs?

- how do I grow top line revenue? increase margins?

- how do I manage weather and disease and market risk?

- how do I accurately manage animal inventory?

Going back to the very first idea from the Apple Watch vs WHOOP analysis, specificity can create big markets. And yet, that leads to the 1st paradox for agtech companies.

The “Everything is the enemy of something” paradox:

the harder you try to have broad appeal by not limiting your product, the harder you make it for target customers to know that your product could be for them. The more you try to appeal to everyone, the less you appeal to anyone.

This paradox shows up as a temptation for tech startups to avoid clearly articulating what their product does for whom, because a prospective customer might have a different use cases.

Then valiantly-struggling-to-get-off-the-ground tech co says HEY NO PROB WE CAN DO ALL THE THINGS. 🤦🏻♀️

Counterintuitively, the idea “our product can do anything” is the biggest enemy of traction because it puts the burden on prospective customers to discover how the product can create value for them.

Specificity can unlock big markets. Getting really clear about the use case and value proposition is how you get really clear in talking to your target customers….but only if you use clear words, the 2nd paradox.

The “Clear Words Paradox” is this:

the more you use jargon (tech or otherwise) to build credibility with target customers, the less credibility you have with your target customers because the words mean nothing.

My high school English teacher used to say ‘words mean things’ – laughably simplistic, but true. Words mean things. Getting the message right means getting specific and using market relevant words with clear meanings.

In my experience, producers tend to be an unpretentious population. Not only does pretentious/superfluous/jargon-y language not help a sales process, it usually hurts the sales process by slowing the conversation down…or killing it.

There’s no benefit in using words that don’t have significance or relevance to our target customers, usually serving the only purpose of making us think we sound smart or innovative. 🤭

With those 2 paradoxes in mind, here are 2 questions to ask yourself about product positioning:

- Am I providing substantive & specific use cases that allows a producer to see how this product solves a specific problem they might have?

- Am I describing the use case in language that is clear?

At first glance, today’s topic is only relevant to those in agtech. But actually my hope is that this gives some helpful language to the innovative producers who engage with agtech startups in the earliest days of beta testing or even early customer discovery. It’s ok, often even really helpful, to tell startups ‘those words mean nothing’ because that’s how they find clarity. I imagine WHOOP struggled through that same process in its early days too!