The natural next questions are, why & how would Tyson do this?

To answer the Why, follow the margin.

Here’s a snapshot of Tyson’s FY Q3 margins across business lines for 2020 vs 2019 from the latest earnings report. Clearly 2020 represents the COVID anomaly, but 2019 is representative of “normal” times.

Takeaway: a good margin target for fresh meat is 5% while further processed should merit 10% margin. With 20% of its business in higher margin further processing, the Hillshire, AdvancedPierre, and several other acquistions over the last 6 years are meaningful to Tyson profitability. Meanwhile Tyson’s competitors are slowly increasing their value added business but largely fighting for that 3-8% margin on fresh meat.

Contrast even the ‘high’ margins of value added with software margin targets ~80+% and hardware margin targets ~50+%. While hardware margins may not be attractive to software investors, when compared against those 5% fresh meat targets, well, they look pretty good.

There’s a compelling case for a commodity company to chase the higher margins of technology.

Now let’s shift to the 3 possible definitions for “become a tech company”:

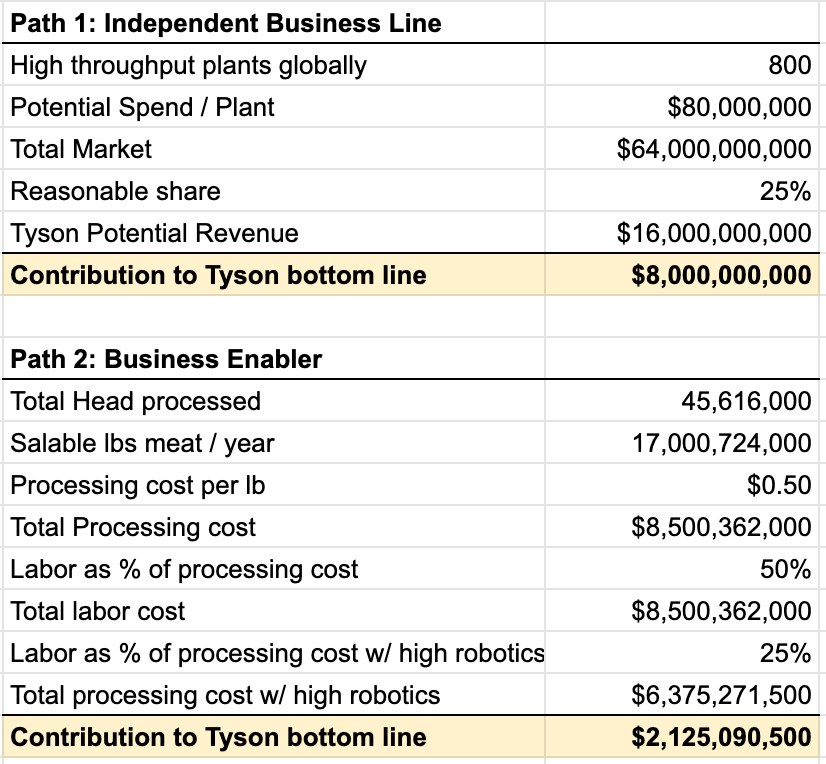

- Tech as a revenue generating business line. Its own business unit, P&L, staff, etc.

- Tech as a core business enabler. Labor represents 50-60% of processing costs. Let’s say Tyson can reduce labor costs by 50% by deploying more robotics in the plant. Apply that reduction across the 45M chickens, 155k cattle, 461k hogs that Tyson processes weekly….

Here’s some (really) crude math around these two paths so before you say that my numbers are wrong, I know. These are wild assumptions for illustrative purposes only to show the (very) rough potential impact on Tyson’s bottom line.

Tyson generated $3.9B EBITDA in 2019 so even if we cut the numbers above in half, these 2 paths represent potential EBITDA growth ranging from 20% – 200%. ??

Now here’s the catch: hardware is difficult. Really difficult. That’s why most VC’s turn and run the second they hear the word ‘hardware’. But if you can navigate the financial & execution challenges of hardware, the light at the end of that tunnel is incorporating software with its oh-so-attractive 80-90% margins. Could Tyson pull that off? Perhaps.

The beauty of hardware is that not only can it improve efficiency of a task, it naturally lends itself to data collection. But what does one do with copious amounts of newly collected data? This is where software gets deployed: to capture, distribute, and analyze the data to derive high value insights. It’s a virtuous cycle, and the hardest part is the hardware. If Tyson can crack the hardware code, the software can (relatively) easily be layered on and the flywheel prints the money. Beautiful.

Which leads to the 3rd path, The Hybrid. The hybrid of the two paths laid out above is Tyson beginning by deploying its own robotics to improve its cost structure in the processing plant, and then also selling the technology to competitors.

But there are a lot of questions as to the viability of the hybrid path given the competitive nature of the industry. Would the Cargills of the world be willing to purchase plant robotics from Tyson that can capture data, and software to analyze that data? Would the Justice Department allow them to do so? I’m skeptical on both accounts.

The rough math indicates this aggressive tech-centric strategy has potential to grow both top line sales and bottom line profit while also mitigating risk for future labor threats like pandemics.

In the first 6 months of COVID-19, Tyson spent $340 million on various measures to protect employees. So a risk mitigation strategy probably sounds good to the Tyson board right about now.

Now that we’ve uncovered the compelling Why and 3 possible How’s to Tyson’s tech strategy, let’s acknowledge the extremely real challenges of redirecting a behemoth like Tyson Foods: the cultural challenges, the technical challenges, the industry challenge, the subject matter expertise challenge, and many more. It will require an absolute Herculean effort if Tyson is to get anywhere close to successful with this transformation.

When I wrote the initial analysis of the Dean Banks selection for CEO, I was honestly feeling pretty bearish on Tyson Foods. But after doing the above analysis, I may hold on to my stock….just in case Tyson’s quasi-ridiculous bet-the-farm strategy pays off.