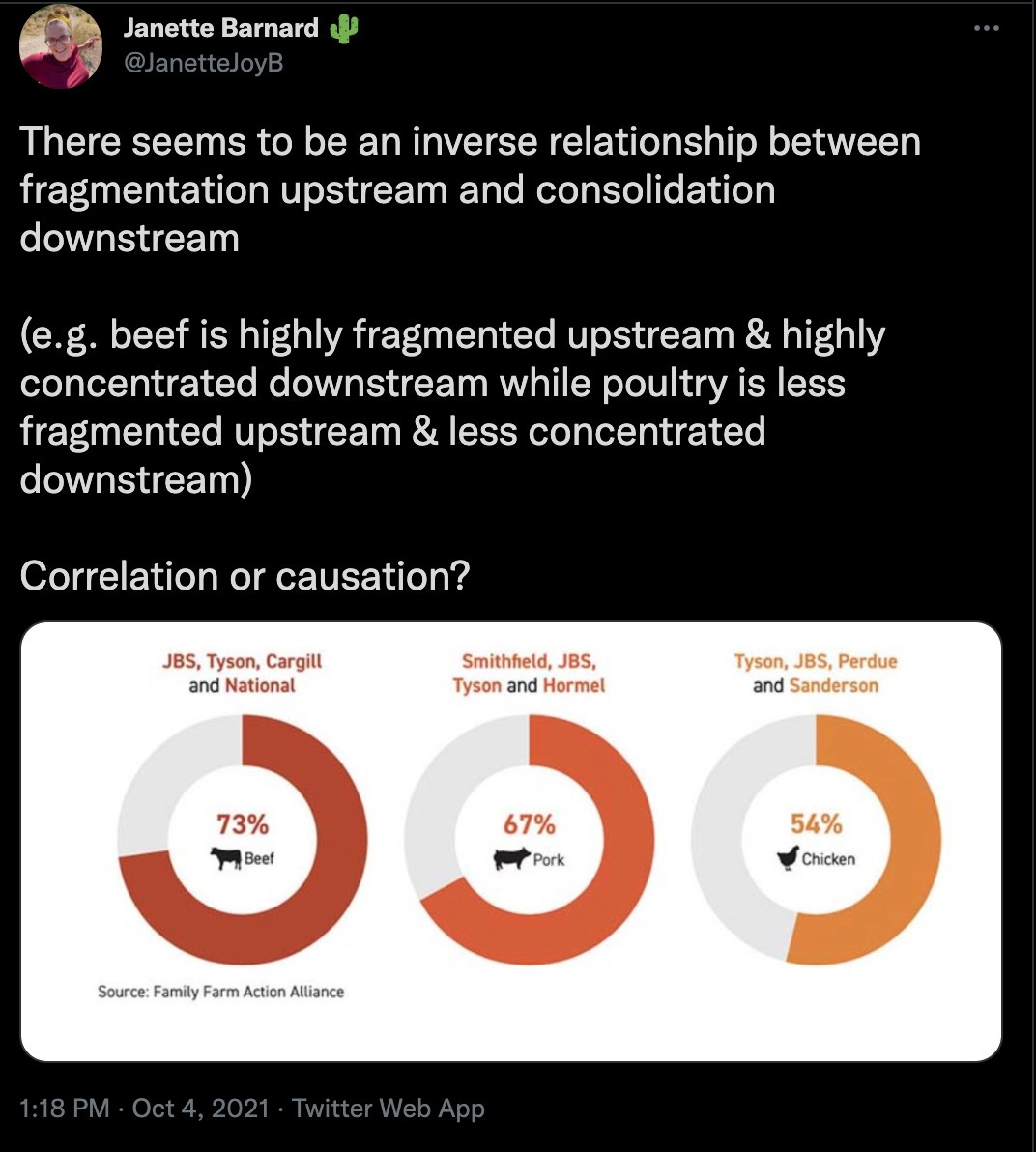

Is beef more concentrated at the packer level because the animals are heavier? More valuable? Or because there’s more’s variation in sourcing? Variation in plant size? Or maybe it’s this:

The answer to why the fragmentation/concentration conundrum exists doesn’t seem to be super obvious, but clearly it’s super complex. Happened-over-time things like packer concentration don’t take place in a vacuum. So simple solutions like the top x processors shouldn’t have more than y% capacity don’t take into account the competing dynamics that led to the current state.

And yet, there is *a lot* of certainty floating around about the topic without much (any?) tolerance for nuance.

But ag isn’t alone in having limited capacity for nuance. (Look, if I was the Debate Commissioner at every presidential debate before a candidate articulated their own position, they would have to summarize the other side’s policy position and say 1 positive thing about it, sans sarcasm.)

There’s another prickly conversation where we need nuance – climate change. I wish people didn’t point to an individual weather events as evidence of climate change. As climate researchers say, it’s not the individual events that are concerning, it is the trends in the data over time – the frequency and severity of extreme weather events. Which means there’s some level of variation that is normal.

Floods, hurricanes, tornados, droughts, heat waves – these are not new events. They were not created by climate change. So pointing at individual weather events as evidence of climate change is either disingenuous or intellectual laziness. Why not highlight more clearly weather events & trends that are within normal variation, versus what’s outside that normal variation?

Another nuance that’s really important is around the distinction of who’s driving change in the industry: consumers or food companies. From Climate + Ag: what gets measured gets monetized (link):

Who’s leading who in climate + ag?

“Consumer wants drive value chain decisions.”

I’ll start by pushing back on the narrative that protein value chains are driven by consumers, on climate or any other topic. Consumers….those nebulous creatures of food commerce who somehow sound like the unknowable inhabitants of an alternative universe when we refer to them. Two flaws with the Consumers-R-In-Control narrative:

- Consumers are not a monolith. Segments of consumers want certain attributes, sub-segments are willing to pay for those attributes. Variation among consumers is no less nuanced than variation among farming systems. Mis-identifying what consumers want and what they will pay for x is as fatal of a flaw as over-estimating how many consumers will pay for x.

- Although staggeringly critical to the system, consumers are not everyone’s customers. Consumers don’t transform supply chains or recalibrate industry norms. Food companies do. Food companies are where the power lies. Brand owners make decisions about how to market meat & milk to their customer: retail consumers. Food companies make decisions about how to market meat & milk, and then where needed those same companies use their scale and influence to set product specs & requirements as they procure raw materials or finished product from a certain set of suppliers. No one is talking about the fried chicken wars of Mar Jac vs Wayne Farms chicken, they’re talking about KFC vs Chick Fil A. The two directional power of influence lies with brand holders across foodservice and retail. Leading brands lead consumers by positioning xyz about their brand that is better than competitors. Food brands tap into consumer trends, but they lead consumer segments with differentiated products. Sometimes those changes are then adopted by other food brands & their supply chains. The massive shift in NAE (no antibiotics ever) production in US poultry is my go to example for this dynamic – when 1-2 major food companies said we will buy NAE chicken, then NAE chicken is what suppliers learned to produce, at scale. So then more food co’s buy NAE chicken. It’s a cycle that starts with a food brand, moving vertically in that supply chain and then expanding horizontally as more food brands (and their supply chains) adopt whatever the thing is.

We oversimplify the value chain when we attribute all influence to consumers, and we underweight the actual centers of leverage.

This week McDonald’s announced their net zero emissions by 2050 commitment. That’s a big deal – we are talking about a legacy, conservative, brand conscious company not some fly by night, here-today-gone-tomorrow brand. This is one of the largest buyers of beef, lettuce, tomatos, pork, potatos, strawberries, etc on the face of the planet. When companies like that start jumping in, it bends the arc towards action – it’s a sign that we’re past the niche-y early adopters and moving right to the middle of the bell shaped curve.

Some interesting context on the McDonald’s announcement from Meatingplace:

Efforts underway since 2018 have resulted in an 8.5% reduction in the absolute emissions of the company’s restaurants and offices and a 5.9% decrease in supply chain emissions intensity measured against a 2015 baseline, McDonald’s reported.

Although the most recent announcement does not specify where in the supply chain the fast-food company will look for its emissions reductions, in an earlier post on its website, the company said, “In collaboration with franchisees, suppliers and producers, McDonald’s will prioritize action on the largest segments of our carbon footprint: beef production, restaurant energy usage and sourcing, packaging and waste. These segments combined, account for approximately 64 percent of McDonald’s global emissions.”

Food companies have leverage, consumers do not.

Another source of leverage is capital. Right now there is an enormous amount of capital (we could put a period there) flowing into climate tech & solutions. More than $33.9 BILLION in venture capital investment has gone into climate tech….in 2021 alone.

Venture capital doesn’t automatically lead to good outcomes and solutions, but it increases the odds of good outcomes when its put behind good founders and good visions and great products. I recently heard someone say “venture capital subsidizes risk taking at scale”.

It’s safe to say that investment in a category tends to be a leading indicator of tech/innovation.

In 2015 Bill Gates founded Breakthrough Energy, a billion dollar fund to “support the innovations that will lead the world to net-zero emissions.” In 2021 Chris Sacca raised an $800M fund to invest in climate tech, with 2 objectives: 1) lower emissions to net zero, 2) get carbon out of the air.

Two interesting quotes on Lowercarbon Capital’s website:

- “Give or take, we’ll need to suck at least a trillion tons of CO2 out of the sky between now and 2100.”

- “Fixing the planet is just good business. Shame and guilt won’t get us there, markets will.”

A few previous comments that are germane to this conversation for livestock:

The extreme positions on either end of the sustainability spectrum will not create actionable, consumer-satisfying, carbon-reducing, market-growing solutions. But nuance…that’s how we find the productive middle ground. Nuance acknowledges that one size does not fit all – what works in geographies that get 40+ inches of annual rain fall won’t necessarily work in areas that get <15 inches. Systematic management changes like transitioning from continuous grazing to intensive rotational grazing are complex, as is anything related to managing the biology of plants or animals.

Regardless of the abundant unknowns about how things will evolve, this whole “climate thing” is not a topic where producers can look away and hope it will disappear. This is a mega trend. There will be winners and losers – my hypothesis is that the difference will be those who collaborate and find workable solutions…or don’t. This is a mega trend to engage, to lead by looking for the ‘and’ solutions…the places of overlap between what’s good for climate related metrics AND for cattle AND for successful cattle operators AND for food companies AND consumers. This is a place to ask questions like, what if? What needs to be true? What opportunities will be created in this mega trend?

Maybe nuance isn’t realistic though – not even because of the formats in which we consume information (140 characters doesn’t leave much room for nuance), but because the human brain can only absorb so much information about so many topics in the midst of living our lives. So sweeping statements and catchy slogans leave us with soundbite driven opinions – and which soundbites we latch onto depends on who we’re listening to.

Anyway, I guess my philosophical point this fine Tuesday is that topics like packer consolidation and climate change are wildly complex with no simple answers, and I’m wary of too much certainty, of the simplistic answers. Anyone peddling simple answers is likely trying to scare or shame to sell something or get a vote (either side).

I think embracing nuance will serve us all well in these discussions.

ICYMI: why is carbon more likely to be a monetizable mega trend than an emotion driven fad? (link)

<insert corporation name> will not be able to buy 2 units of sustainability to offset 2 units of un-sustainabillity. But, <insert corporation name> will likely be able to buy 2 units of carbon sequestration to offset 2 units of carbon emissions.

As more companies make net-zero commitments around carbon and seek to offset carbon in their supply chains, carbon markets are the likely place to turn. To make this carbon economy go, the entire structure will have to be underpinned by rigorous standards of measurement and verification. Sound methodology and precision processes are the only way for carbon markets to deliver on the promise for participants and their investors, customers, and consumers.

Another concept bubbling up is carbon labeling on food. Only high end, niche brands are pursuing carbon labeling now, but will this become a more widely adopted practice? The concept behind these labels is numerical representation of the carbon involved in production….the (potentially) magical word for livestock producers is “numerical”. To the extent that sound methodology and high integrity math drive carbon labeling, it represents an opportunity for livestock producers to win by numerically capturing the net positive carbon impacts of livestock production.

People way smarter than me can go deeper on carbon markets and carbon labeling. My point is simply this:

Carbon could be the real deal for producers because both B2B carbon markets and consumer facing carbon labeling on food would require data driven approaches to drive an actual functioning net zero carbon economy based on measurements.

I’m interested in all things technology, innovation, and every element of the animal protein value chain. I grew up on a farm in Arizona, spent my early career with Elanco, Cargill, & McDonald’s before moving into the world of early stage Agtech startups.

I’m currently on the Merck Animal Health Ventures team. Prime Future is where I learn out loud. It represents my personal views only, which are subject to change…’strong convictions, loosely held’.

Thanks for being here,

Janette Barnard